MORE FOIA MEMOS: The Fed’s 2013 Treasury Default Memo. Just in Time for Another Round of Debt Ceiling Politics

Please recommend an institutional subscription to your academic library or employer (details here)

The debt ceiling was unsuspended January 1st of this year which means the debt ceiling is back. According to now-former Treasury secretary Janet Yellen, they began using “extraordinary measures” to avoid hitting the debt ceiling as of today. As regular readers know, I’ve long commented on the absurd political economy of the debt ceiling. I’ve lodged successfully FOIAs and released multiple memos related to the topic. In fact, I’ve written so much about the debt ceiling. that I think it's worthwhile to simply provide a chronological list of all the previous pieces I’ve written in recent years. To start with, The Guardian piece is my most basic primer on the Debt Ceiling and the recurrent concerns about debt ceiling driven default. But all the pieces, especially my Politico Op Ed, are worth a look.

The Guardian: The case for minting a $1tn coin to deal with America’s debt ceiling

Financial Times Alphaville: The Fed will have to accept the $1tn platinum coin

Financial Times Alphaville: Three questions for Fed Chair Jay Powell

Politico: Biden Can Steamroll Republicans on the Debt Ceiling And Fed Chair Jay Powell won’t interfere.

Notes on the Crises: I Got the Fed to Release its 2011 “Treasury Default” Playbook. Here’s What it Says and Why it Matters.

Notes on the Crises: More FOIA Findings: The New Nixon Administration’s Debt Ceiling Dilemma and the Federal Reserve’s Solutions

Notes on the Crises: Paul Volcker’s Secret December 1973 Phone Call to Fed Chairman Arthur Burns Revealed

Of course, the concerns about the debt ceiling aren’t anywhere near as serious as they were in 2023. That’s because Donald Trump was inaugurated as president yesterday. As my Politico Op-Ed covers, the debt ceiling has become a tool for Republican congresspeople to use the threat of default to push through their preferred fiscal policies. Their need, and their willingness, to do this under a Republican president is obviously radically lower. This is especially true when that president is Donald Trump, who enters his second term as the absolute undisputed leader of the Republican Party. Even if some of the most “hard-line” Republicans hold out, GOP leadership will likely be able to find Democratic votes. After all: Democrats are not comfortable using those same “hardball tactics”. Nor do they show the same partisan unity against Republican presidents that GOP congresspeople have shown against Democratic presidents in recent decades.

Nevertheless, the struggle over the debt ceiling may take a significant period of time given the razor-thin Republican congress. The time that “conventional extraordinary measures” buy may not be consistent with that full process playing out. So while the debt ceiling is in the news, it's worth taking another look at the topic.As it happens, I have more successfully FOIAed memos to release. These are follow ups to the “2011” Treasury default memo. In September 2023, I gave the memo a close read, and set them against the 2011 and 2013 FOMC transcripts that seemingly discussed it in the context of the debt ceiling fights going on in those years. What I realized is that despite having the same name and having largely the same content, the 2013 memo under discussion was a different memo, that had subtly different numbering. I thus decided to FOIA for that memo, too. After a year of delays, the FOMC FOIA office gave me access at the end of September.

Unsurprisingly, the 2013 “Potential Policy Responses to the Debt Ceiling” memo by Bill English and Simon Potter is pretty similar to the 2011 “Potential Policy Responses to the Debt Ceiling” by Bill English and Brian Sack. Yet the differences between them are revealing. It is also interesting reading what has evolved from “first draft thinking” to “Federal Reserve consensus” in the intervening two years. In this respect, the memo’s summary of the status of the “first five” options is worth quoting at length:

We begin by describing how delayed payments could affect five routine policy actions that are permissible under the Federal Reserve Act and fall within the current authorization of the [New York Fed Trading] Desk and the authority of the Reserve Banks. The transcript of the Committee discussion in 2011 suggests that there was broad support for these types of actions, should they prove necessary, without any change to the current procedures. Underlying each of these actions is the premise that the Federal Reserve would continue to accept Treasury securities with delayed payments in these transactions at their (potentially reduced) market values and on the same terms that apply to other Treasury securities. This approach seems appropriate because we continue to anticipate that after a relatively short delay, all Treasury securities will be paid in full, and so the securities remain very low risk. These five actions could help the market cope with the pressures that may emerge in the event of a technical default

In short, the first five options had by this point become the standard toolkit and they were meant to avoid the fallout from a “technical default” i.e. one that lasted a short period of time. As I pointed out back in 2023, “Option 1” involves continuing to buy defaulted treasuries as if they were not defaulted treasuries. And that means this has remained consistently uncontroversial to Federal Reserve officials.

Options 6 and 7 in the memo are engaging in repurchase agreements, and reverse repurchase agreements to prevent repo lending rates from going negative (or going too sharply positive). Recall that repo agreements are essentially collateralized lending with “favorable” treatment for creditors in bankruptcy. These options are the same as they were in 2011, though there are more details about how they would work and the tone of the descriptions suggest they were very favored by Fed s. Notably, though the memo ends up merely suggesting that they warrant “serious consideration”... just like last time!

The most interesting part of the discussion is in fact a brief discussion of legal issues. According to the memo “Such operations could also be authorized by the Chairman to address ‘temporary disruptions of U.S. dollar funding markets’ of a ‘highly unusual nature,’ although the Chairman would consult with the Committee if feasible before taking such a step”. We learn in a footnote that “The Chairman’s authority in such cases was added to the Authorization for Domestic Open Market Operations in January 2013.” meaning the Federal Reserve system had quietly set the stage for engaging in more aggressive support for the treasury market and the wider financial system at a moments notice.

It is only with Option 8 that this memo truly diverges from the 2011 one. In 2011, Option 8 was a specific 13(3) lending facility meant to prop up money market mutual funds. The memo explains why:

Finally, the 2011 memo considered the possibility for a new liquidity facility, specifically one targeted to provide support for money market funds (action 8 in the 2011 memo). The transcript from the August 2011 FOMC meeting suggests that such an approach had very little support. Thus, this option is not being considered by the staff at this time. Additionally, staff believes that market operations targeted at purchasing Treasury securities with delayed payments (and perhaps those seen by some market participants as at risk for delayed payments), potentially in combination with RPs, could be a more effective way to provide liquidity to money funds than a lending facility. Such actions, especially if taken before severe market dislocations had pushed prices down substantially, could stem concerns over the viability of money market funds facing large redemptions

In other words, this option has simply disappeared because the staff gleaned from the 2011 FOMC meeting that discussed the earlier memo that FOMC participants were against it. It’s worth noting that in 2020 the Federal Reserve brought back the Money Market Mutual Fund Lending Facility (MMLF).

Which brings us to the last two options. Whether numbered Option 9 & 10, as in 2011, or numbered Option 8 & 9 as in 2013, these are the most explosive options. These options essentially involve a commitment to, as much as possible, prevent any wider knock-on effect from a debt ceiling driven treasury default by expanding the Federal Reserve’s balance sheet to absorb defaulted treasuries. Just like the FOMC meetings discussing these options, the memo is skittish about their use. However, it makes absolutely clear that these options are “on the table” and given that one option was removed from the memo while these options were not, the Fed clearly remained willing to use this option if it felt it needed to.

The memo states:

If these pressures were sufficiently large, the Committee might see such purchases as appropriate to support financial stability and foster its macroeconomic objectives. However, such an approach would insert the Federal Reserve into a volatile political situation and could raise questions about its independence from debt management issues faced by the Treasury. Thus, the staff assumes that the FOMC would not be interested in pursuing these options, but they are presented for completeness.

The cover letter to these memos, also released to me by the FOMC FOIA office, makes the Fed’s willingness (however reluctant) to use these options even clearer. Entitled “Background Documents and Questions for Discussion of the Debt Ceiling”, the final question states:

In 2011, the Committee set a high threshold for actions 8 and 9 (purchase operations and outright CUSIP swaps to remove Treasury securities with delayed payments from the market). Such operations could be used to support financial stability and limit the risk of adverse effects on the economy. How would you balance those possible benefits against concerns about the appropriate role of the Federal Reserve in issues related to the fiscal authorities?

The Federal Reserve wants to avoid being in a situation where it has to overtly diffuse the crisis, but they will take over those duties, if push comes to shove.

As I discussed in late 2023, the legal memo on accounting gimmicks to avoid the debt ceiling which involved the Fed written by Howard Hackley in 1969 provides quite a wide latitude for rationalizing Federal Reserve actions to avoid default. Even actions that “would constitute a direct extension of credit to the Treasury by the Federal Reserve” can be “legally defensible as not being designed primarily to aid the Treasury but as intended to avoid developments that would have an adverse impact upon the ‘credit situation of the country.’” This clearly remains as the Fed’s guiding legal thinking, even if they carefully hid it for decades.

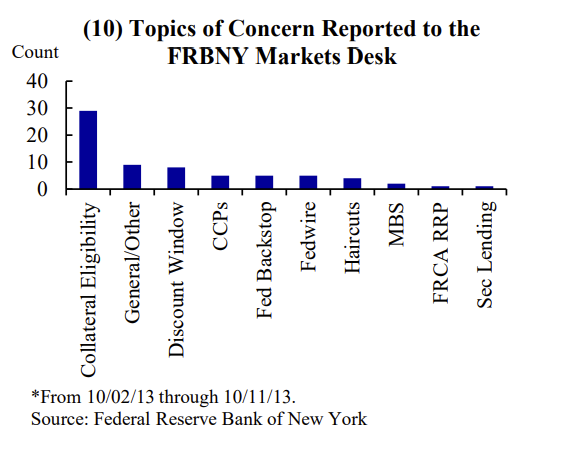

The final memo I got hold of is entitled “Impact of Debt Limit Concerns on Financial Market Conditions” by Fabio Natalucci and Kevin Stiroh. This memo has a lot of real time financial detail which is interesting and worth comparing to public accounts of developing financial market stress. However, for today I will point to the one part of it which I think is of lasting interest. That is the survey the New York Fed’s trading desk apparently started keeping on October 2nd, of the type of questions it was getting from market participants. As the graph shows, the questions were primarily concerning what would be accepted by the Fed as collateral in case a treasury default actually happened.

Despite the 2011 memo being around for some time, it has only unevenly been absorbed by debt ceiling discourse. The recent Congressional Research Service report on the Debt Ceiling is one of the few sources which cite the 2011 memo, although the authors do not fully grasp its import. The recent Government Accountability Office report fails to cite it even though it provides a brief (and misleading) discussion of its contents through the FOMC transcripts.

Now that I’ve publicly released the 2013 memos and it is clearer than ever that the Fed will step into stem financial stability concerns, it's worth having an honest conversation about the debt ceiling while the stakes are lower under a Trump presidency. Between Trump’s meme coin and the proposed “Strategic Bitcoin Reserve”, the Trillion dollar platinum coin has never looked more like the “adult in the room”

Sign up for Notes on the Crises

Currently: Comprehensive coverage of the Trump-Musk Payments Crisis of 2025